1. What an ITC actually is

For Ontario businesses paying 13% HST on every purchase, input tax credits are how you get that money back. An input tax credit (ITC) is the GST or HST you paid on business purchases, claimed back from CRA on your next return. CRA ties every ITC to commercial activities — the parts of your business that produce taxable or zero-rated sales.

It's the easiest GST/HST concept to explain and the easiest one to mess up in practice. The credit looks simple, but only when the purchase really belongs to the business and the paperwork holds up.

If you want the bigger GST/HST framework around it, start with our GST/HST guide. This post is the receipts-and-claims version of that story.

2. Who can claim one

Only a registrant can claim an ITC. A registrant is a business that has a live GST/HST account with CRA.

CRA adds three conditions: you must be a registrant during the reporting period when the tax was paid or became payable, you must have paid or owed the tax yourself, and the purchase must have been for use in your commercial activities. Most cleanup jobs fail because one of those three got missed in the rush.

If you're not registered yet, read our GST/HST registration guide first. No registration usually means no ITC.

3. Receipts and documentary proof

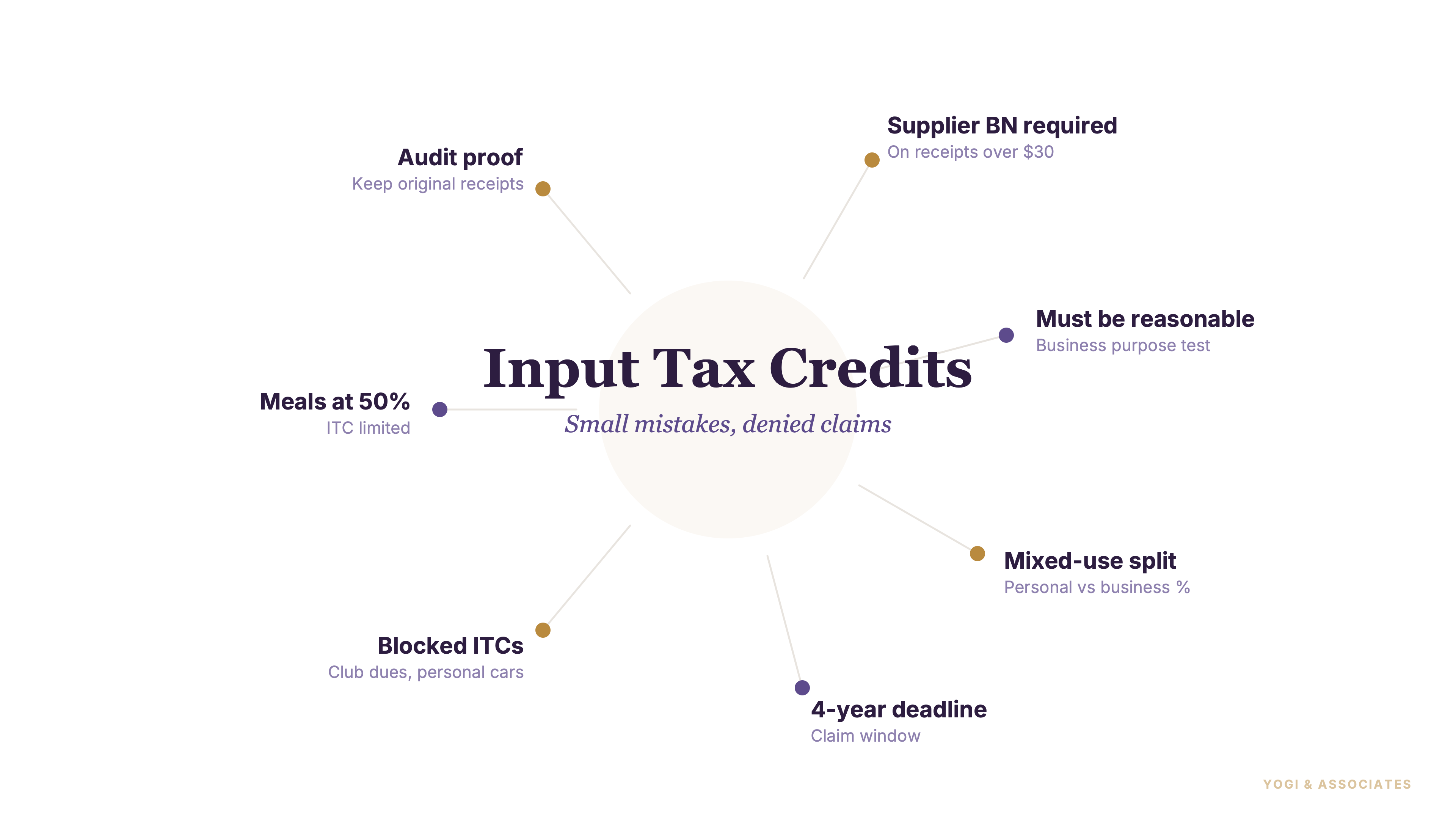

This is where real money gets lost. CRA has three receipt tiers, and the documentation bar rises with the dollar amount.

Under $30: basic supplier details, the date, and the total paid. $30 to under $150: add the supplier's GST/HST registration number and the tax details. $150 or more: full supporting information about the transaction and the tax shown.

A missing supplier number on a $600 invoice can turn a legitimate expense into a denied claim — and CRA catches that quickly on review. Fix the receipt discipline before you file, not after.

4. How long you have to claim

Most registrants have four years from the due date of the return where the ITC could first have been claimed. CRA cuts that to two years for listed financial institutions and certain specified persons.

The main specified-person test is size. The shorter two-year limit can apply when annual taxable supplies exceed $6 million.

Missed ITCs are one of the most expensive cleanup jobs in indirect tax. Our HST filing service exists partly because these deadlines are easy to ignore until they bite.

5. Meals and entertainment limits

Most business meals don't get a full ITC. CRA applies the same 50% restriction that normally applies for income tax purposes.

So even if the meal was legitimate, only 50% of the GST/HST is usually claimable. This catches owners because the receipt feels fully business-related, but CRA still caps the claim.

This is also one of the places where your GST/HST logic and your income tax logic need to agree. Our small business deductions guide lines those two sides up.

6. Capital property and mixed use

Mixed-use expenses have to be apportioned. You can only claim the GST/HST that matches the purchase's use in your commercial activities.

Operating expenses follow a tiered rule. 90% or more commercial use usually means a full ITC. 10% or less means no ITC. Anything in between gets apportioned on a fair and reasonable basis.

Capital personal property works differently — it's a cliff, not a slope. Take a business vehicle: say you use it 60% for work and 40% personal. Because you're above the 50% commercial line, the ITC is available on the business portion. Drop that to 50% or less and the claim disappears entirely. Not reduced. Gone.

Watch that threshold whenever the mixed-use ratio shifts. A car that was 60% business this year can quietly slide to 45% next year — and the ITC treatment flips with it.

7. Common ITC mistakes

The classic errors are boring but expensive. Missing supplier details, personal expenses mixed into business costs, and old claims filed after the time limit show up on nearly every cleanup file we see.

Double-claiming is another problem, especially when bookkeeping gets caught up in batches. ITC reviews go best when the receipts, the ledger, and the return get checked together — not one at a time.

If your books still live in screenshots, scattered PDFs, and half-coded expenses, fix that before the return goes out. And if you're also juggling self-employment reporting, our self-employed tax guide is the right companion read.

Not sure if your last return left ITCs on the table — or over-claimed ones CRA could bounce? We review receipts, timing, and mixed-use percentages for GTA owners every week. Before you file, not after.

Book a Free Consultation