1. How Canadian tax brackets actually work

Here's the part most people miss. Your tax rate isn't one number. It's a stack of rates, each applied to a slice of your income.

Say you earn $100,000 in Ontario. The first $53,891 gets taxed at the lowest provincial rate (5.05%). The next slice gets taxed at 9.15%. And so on.

Federal tax works the same way on top. Nobody pays their top rate on their whole income — not even people in the top bracket.

So when you hear “marginal rate,” that's the rate on your next dollar earned. Your average rate — what you actually pay on everything — is always lower. that one distinction clears up about half the confusion people have about their T1.

2. Ontario brackets for 2026

Ontario indexed its lower brackets by 1.9% for 2026. The two highest bracket thresholds ($150,000 and $220,000) are not indexed — they've been frozen there for years.

- 5.05% — on the first $53,891 of taxable income

- 9.15% — on income from $53,891 to $107,785

- 11.16% — on income from $107,785 to $150,000

- 12.16% — on income from $150,000 to $220,000

- 13.16% — on income above $220,000

These are provincial rates only. They're not the full story. Federal tax layers on top, and the Ontario surtax sneaks in at higher incomes — we'll get to both in a minute.

3. Federal brackets for 2026

The big federal change this year is the lowest bracket. It dropped from 15% to 14% effective January 1, 2026. That's a real cut on your first dollar of income, not just an inflation adjustment.

The rest of the federal rates stayed put. But all the thresholds were indexed up by 2.0% for inflation.

- 14% — on the first $58,523

- 20.5% — on income from $58,523 to $117,045

- 26% — on income from $117,045 to $181,440

- 29% — on income from $181,440 to $258,482

- 33% — on income above $258,482

And here's the part worth pausing on. A 1% cut at the bottom doesn't sound like much. But it applies to the first $58,523 of everyone's income.

So every Ontario taxpayer — from minimum wage to top bracket — saves up to $585 in federal tax in 2026 just from that change alone.

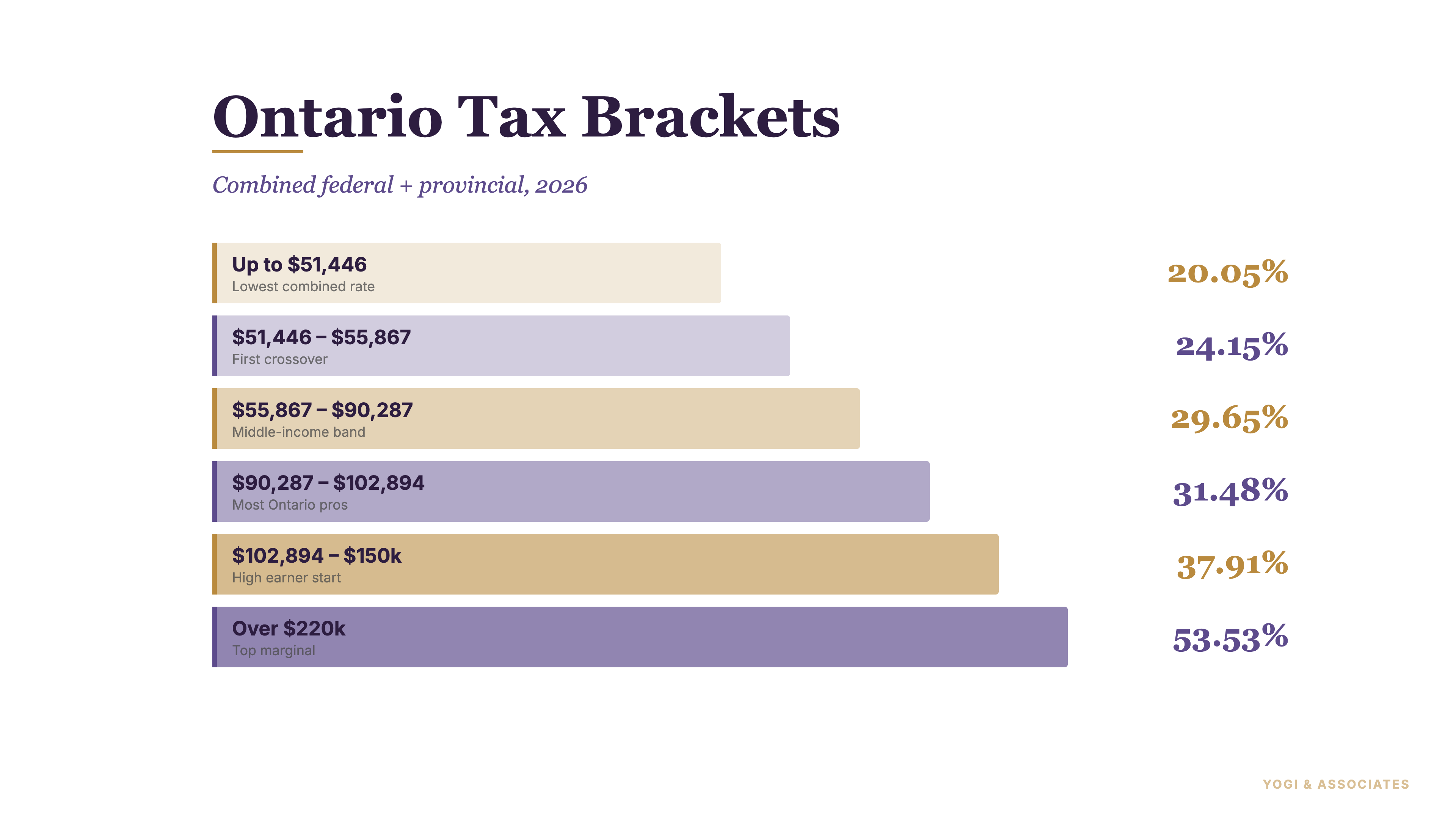

4. Combined Ontario + federal rates

Most people just want to know the combined number. That's the rate on your next dollar earned, once you add federal + provincial together. In 2026, here's roughly where the combined marginal rate sits in Ontario:

- Around 20% on the lowest slice of income (the overlap of the 14% federal and 5.05% Ontario brackets)

- Low-to-mid 30s% through the middle-class range ($55K–$110K)

- Low-to-mid 40s% once you cross into six figures

- Around 53.53% on income above $258,482 — the top combined rate

53.53% is the number worth remembering. Because it's not just the top bracket — it's what happens when Ontario's surtax stacks onto the 33% federal and 13.16% provincial rates. Every extra dollar at that level, more than half goes to CRA and the Ontario government.

So if you're a business owner deciding between a salary and dividend payout, those combined marginal numbers are what you're actually comparing against — not the posted federal rate alone.

5. The basic personal amount

The basic personal amount (BPA) is the slice of income that's effectively tax-free. Everyone gets it. You don't claim it — it's built into the T1.

For 2026:

- Federal BPA — up to $16,452 (it phases down for high earners)

- Ontario BPA — $12,989 (flat)

Technically these aren't “tax-free zones.” They're non-refundable tax credits calculated at the lowest bracket rate. But the math works out to the same thing for most people: the first ~$13K–$16K of your income doesn't generate any tax.

Plus, the federal BPA got a real bump for 2026. It's higher than last year, and combined with the 14% cut, the first chunk of income is meaningfully cheaper to earn in 2026 than it was in 2025.

6. The Ontario surtax nobody warns you about

This is the one that surprises people. Ontario has a surtax — a tax on tax — that kicks in at middle-income levels. It's not a separate bracket. It's a percentage on top of the Ontario tax you already owe.

For 2026:

- 20% surtax on the portion of Ontario tax over $5,818

- Additional 36% surtax on the portion of Ontario tax over $7,446

So once your Ontario tax bill crosses $7,446, you're paying a 56% surcharge on every extra provincial tax dollar. That's what pushes the combined top marginal rate up to 53.53% — the surtax is doing most of the work.

But here's the thing. The surtax starts biting at around $86,000 of taxable income for a single filer. So plenty of mid-career professionals in Toronto are paying it without ever realizing there's a “tax on their tax.” It just shows up as a bigger number on line 42800 of the T1.

7. What this means for your T1

Knowing the brackets is step one. Using them to make smarter decisions is where most taxpayers leave money on the table.

- RRSP contributions hit hardest at your top marginal rate. A $10,000 RRSP contribution saves you $3,500+ if you're in the 35% bracket, but over $5,000 if you're at the top. Timing matters.

- Split income with your spouse if you can. Pension income splitting, spousal RRSPs, and family trusts exist because moving income from a high-bracket spouse to a low-bracket one is legal tax savings. Not every household can do it. But many can.

- Watch the surtax threshold. If you're close to $86K taxable income, an RRSP contribution or a charitable donation can drop you below the first surtax tier. The savings are real.

- Realize capital gains in the right year. Only half of a capital gain is taxable (at time of writing), but that taxable half gets stacked on top of your regular income. A $100K gain in a low-income year costs much less than the same gain in a peak earnings year.

- Use the TFSA for high-rate investment income. Interest and foreign dividends are taxed at your full marginal rate. Inside a TFSA, they're not taxed at all.

And if none of this looks like a fun Saturday night, that's fair. Planning a T1 around brackets is the kind of thing we do day-in, day-out.

Want the full picture on personal tax filing in Canada? Start with our tax preparation guide. Or if you'd rather skip the homework, we handle personal tax filing for Ontario families every spring.

Not sure what your real marginal rate is, or how to plan around it? We do T1 returns for Ontario families every spring. Let's take a look before April gets here.

Book a Free Consultation