1. The real question isn't salary vs dividends

Most owners come in asking which one saves more tax. But that's the wrong way in. Canada's tax system is built around an idea called integration — the total tax you pay should be roughly the same either way.

Roughly. Not exactly.

The gap is usually small. And it's not where the real money lives.

The bigger question is what you want the rest of your financial life to look like.

RRSP room. CPP. Mortgage applications.

Disability coverage. Cash flow.

Those are the things that actually move based on which lever you pull. So that's where we start every conversation.

2. How paying yourself a salary actually works

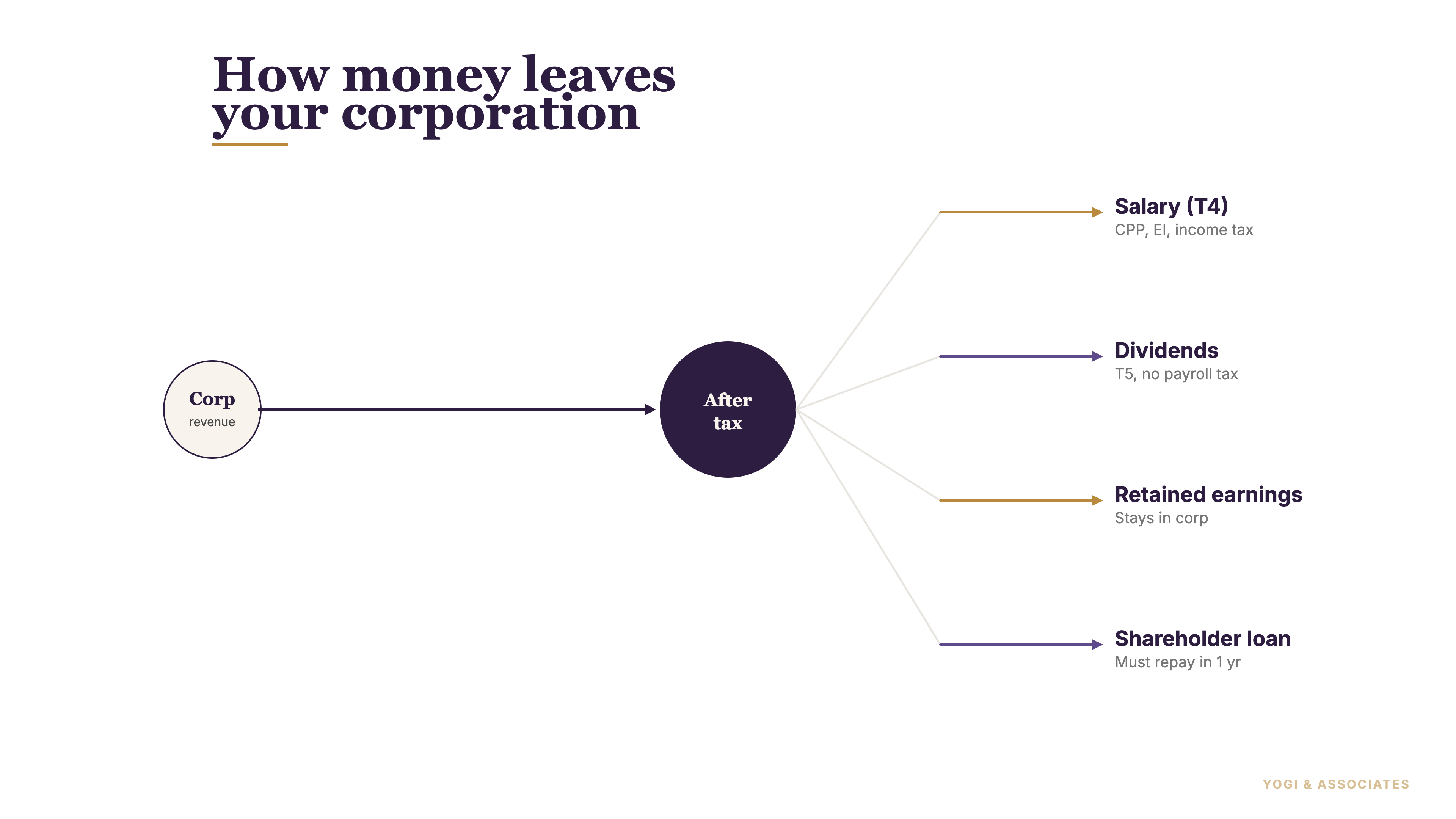

When your corporation pays you a salary, it's treated like any other employee wage. The company registers a payroll account with CRA, runs you through payroll, and remits source deductions every month.

You get a T4 at year-end. The corporation deducts the salary as a business expense. And that's the first thing that matters — salary reduces corporate taxable income, so the corporation pays less tax.

But salary isn't free. Here's what comes with it in 2026:

- CPP on both sides. The employee half comes off your paycheque. The employer half comes out of the corporation. For 2026, CPP covers pensionable earnings up to $74,600 (the YMPE), and the new CPP2 tier covers earnings between $74,600 and $85,000 at 4% for each side. Self-employed owner-managers on payroll end up paying the full cost either way.

- EI usually doesn't apply. If you own more than 40% of the voting shares, you're generally exempt from EI premiums. That saves some friction — but it also means no EI benefits if the business slows down.

- Source deduction remittances. Income tax gets withheld and sent to CRA on a schedule (monthly for most small corporations). Miss a remittance and the penalty clock starts immediately — we wrote about how CRA interest and penalties work and payroll remittances are one of the fastest-growing problems on any file.

- T4 slips and WSIB filings. Extra compliance at year-end. Not hard, but not nothing.

So yes, salary is a real deductible expense. But the CPP cost and the paperwork are real too. Of salary less as a “tax strategy” and more as an operating decision with tax effects.

3. How paying yourself dividends actually works

Dividends are different. They're a distribution of after-tax corporate profit. The corporation pays its tax first, then pays you what's left.

There's no payroll account. No source deductions. No T4.

Instead you get a T5 slip at year-end reporting the dividend amount. That's it for the corporate side of the paperwork.

On your personal T1, though, dividends look weird. Canada taxes them using a gross-up and a dividend tax credit (DTC). The gross-up — the government inflating the dividend before taxing it — is meant to roughly reflect the corporate tax already paid.

Then the DTC gives you credit for that corporate tax. It's awkward to read on a return. But the math is supposed to land you in about the same place as if you'd earned the income personally.

Two flavours to know:

- Non-eligible (ordinary) dividends — paid from profit that was taxed at the small business rate. Federal gross-up is 15%, and the federal dividend tax credit is 9/13 of the gross-up amount. Ontario has its own provincial DTC that stacks with the federal one. This is what most Ontario owner-managers end up paying themselves.

- Eligible dividends — paid from profit that was taxed at the higher general corporate rate. Bigger gross-up, bigger credit. Rarely what comes out of a small CCPC unless the company is earning above the $500K small business limit.

Plus there's no CPP. That's a real savings year to year. But it's also a real gap in your retirement picture if you were counting on maxing out CPP benefits later.

4. The integration idea (and where it breaks)

Canadian tax policy tries to make salary and dividends come out to about the same total tax bill. That's integration in one sentence.

The way it works: if the corporation pays the small business rate (around 12.2% combined in Ontario for 2026), and then you pay personal tax on the dividend with the dividend tax credit offsetting part of it, the total should be close to what you'd pay if you'd earned the income as salary directly.

Close. Not identical. In Ontario, the small gap usually slightly favours dividends at lower personal income levels and slightly favours salary at higher ones.

But we're talking a percentage point or two. Not life-changing.

And here's where integration breaks. It assumes you're taking all the money out in the same year the corporation earns it. If you leave profit inside the corporation — to reinvest, to save for a slow year, to build retained earnings — the math changes.

That's where a corporate structure starts doing real work.

5. RRSP room and CPP — the hidden tradeoff

Here's the part most comparison charts skip. Salary creates things dividends can't.

RRSP contribution room is 18% of prior-year earned income, to a dollar cap. Salary counts as earned income. Dividends don't.

So if you pay yourself $100,000 in salary this year, you generate $18,000 of RRSP room for next year. Pay yourself $100,000 in dividends? You generate zero.

That matters if the RRSP is a core part of your retirement plan. a lot of incorporated owners feel clever for skipping payroll — and then realize a decade later that their RRSP is frozen at the number it was before they incorporated.

CPP is the same story. CPP retirement benefits are based on how much you contributed over your working life. Dividend years are blank years for CPP purposes.

Some owners are fine with that. Plenty aren't, especially once they look at what the enhanced CPP actually pays out in retirement.

There are a few other things salary unlocks: childcare expense deductions need earned income, individual pension plans (IPPs) need T4 income, and mortgage underwriters generally like seeing a T4 more than a T5. These aren't deal-breakers on their own. But stacked together they tilt a lot of decisions.

6. What we usually recommend

There's no universal answer. But here's the rough framework we walk clients through, plain and simple:

- Start with how much you need to live on. Not what sounds clever — what actually goes out of your personal account each month. That's your baseline draw.

- Decide if RRSP room matters to you. If yes, you need enough salary to generate the room you want. If the RRSP isn't part of your plan, dividends carry less weight there.

- Think about CPP on purpose. Opting out of CPP by going pure-dividend is a real choice. We want clients to make it deliberately, not by accident.

- Leave something inside the corporation if you can. Retained earnings taxed at the small business rate (12.2% combined in Ontario for 2026) give you a powerful place to save — as long as you're not parking too much passive investment income there. That's a separate conversation.

- Top up with dividends for the rest. Once salary is covering the things only salary can cover, dividends fill in the gap without the payroll overhead.

And for context — we've been setting up owner-manager compensation for Mississauga and Ontario businesses since 1998. The “right” mix has moved around as rates and CPP rules have changed. But the decision framework has stayed the same: figure out what the money is for, then choose the mechanism that gets it there cleanly.

Want the bigger picture on Canadian tax filing? Start with our tax preparation guide.

For personal brackets and marginal rates that feed into the dividend math, read our Ontario tax brackets post. And if you're pulling money out of the corporation another way, you'll want to know about the 15-month shareholder loan rule too.

Or if you'd rather skip the homework, we handle corporate tax and personal tax together for incorporated owners across Ontario.

Not sure what mix of salary and dividends makes sense for your corporation this year? We run this planning for Ontario owner-managers every fall and every spring. Let's look at the numbers together.

Book a Free Consultation